LookFar Ventures18 November 2016

Demystifying Startup Finance Part V: Anti-Dilution Provisions

This is Part 5 in our Demystifying Startup Finance series. Follow the links to read part 1, part 2, part 3, and part 4.

Previously we walked through dilution with a simple cap table. Simple in this case means that every round on the table is an up round, and it ignores ESOPs, discounts, warrants, valuations, and multiple terms that can be set in an investment.

But what happens if real life intercedes, and a company sees a down round? Investors face not only dilution of the number of shares held, but a decrease in value of their shares. Put together, the two can combine for a considerable loss on their investment.

Unless their term sheet included an anti-dilution provision.

Anti-Dilution provisions are sometimes placed in the terms of an investment to protect the investor from significant loss due to dilution in a down round. They give investors the right to increase the number of shares they hold by comparing the amount of shares they originally held, the price-per-share at the time of their investment, and the new lower price-per-share.

Anti-Dilution provisions increase the conversion rate at which a preferred share holder’s stock converts to common shares in the event of an exit. When purchased, preferred shares have a 1:1 ratio compared to common shares. Conversion from preferred shares to common shares typically happens in the event of an IPO or when an investor stands to realize greater profit with a greater number of common shares in a liquidation or acquisition event.

Full Ratchet and Weighted Average Provisions

In a Full Ratchet provision, the initial investment is converted to the number of shares afforded at the new price-per-share for the same amount. Because founders’ shares are rarely preferred shares, the same luxury is not afforded to them. The number of shares founders hold will remain the same, even as the new shares are issued to participants of both the down round and Full Ratchet provision holders. Therefore, founders’ percent ownership will be significantly decreased.

For Full Ratchet provisions, the conversion price is the price-per-share of the down round.

Use the conversion price to find the number of shares held post down round.

![]()

Or simply:

![]()

The larger the amount of shares sold, the lower the price the investor is able to convert his or her shares to, and therefore will wind up holding more shares. If few shares are sold in the down round, the investor has the right to fewer additional shares, therefore leaving more equity in the hands of the founder.

There are two basic types of weighted-average provisions: broad-based and narrow-based. Both use essentially the same formula to find the conversion price; however, the broad-based formula considers all common shares, including outstanding shares, warrants, options, and preferred shares convertible to common. The narrow-based formula considers only the shares currently outstanding.

As our cap table is lacking warrants and options, we will examine the broad-based conversion price. Here’s the formula:

![]()

Where shares issuable at old price-per-share is equal to:

Where initial price-per-share is the price an investor paid during the round the share was purchased in. Plugging that and the conversion price into the following formula will get you the number of post-conversion shares the investor holds.![]()

Or simply:

![]()

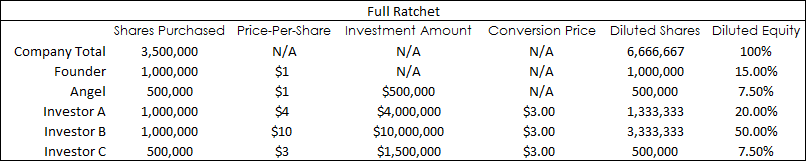

Let’s examine the effect of a down round on our company from the dilution example. Let’s say our hypothetical company’s price-per-share pre-money for their Series C is $3/share, down from the $10/share price for Series B, and $4/share for Series A.

**for ease of understanding, angel investors in this example have no liquidation or anti-dilution protection.

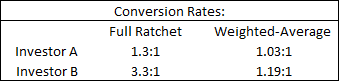

Regardless of which provision is utilized, the impact of exercising it can be measured as following:

![]()

**displayed as a ratio

Therefore the conversion rates vary based on price-per-share on initial investment and provision type:

It is important to note that the effects of anti-dilution provisions can be significantly more taxing on founders if the incoming investor does not agree to the change. This results in infinite regress or the “death spiral” of anti-dilution. Death spirals occur when pre-existing and new investors continue to lower their price-per-share to eliminate the effects of dilution on their equity until an equilibrium price is reached.

Due to the severity of the impact these provisions can have on a company, it is important to understand how the addition of these provisions will affect founders and investors. As you can see, full ratchet provisions will always result in a higher dilution for common stock holders than weighted-average, making them a riskier proposition for founders.

Exact terms of how anti-dilution provisions are executed differ by the terms of the covered investments and subsequent investments. Be sure to consult your attorney regarding the specifics of your investments.

Written by

How to Build Your Magic Machine: A primer on technical development for Startup Founders

How to Build Your Magic Machine: A primer on technical development for Startup Founders  Net Neutrality in the Southeast: Why Emerging Hubs Should Fight for Title II

Net Neutrality in the Southeast: Why Emerging Hubs Should Fight for Title II